Methane – the rise and fall of molecular twins

Caroline Randall

Marketing Manager

Since the demise of king coal, natural gas has become the UK’s dominant energy source accounting for 35% of total UK energy demand in 2024. It’s the country’s primary source of heat and a key fuel in electricity generation; it is increasingly used as fuel for heavy goods vehicles, and acts as a critical source of hydrogen in chemical manufacturing.

However, its dominance is on the wane. UK demand for gas peaked in 2004 at 1,132TWh and despite a production rally in the mid-2010s, consumption dropped to 689TWh in 2024.

Declining demand for natural gas.

Natural gas is primarily methane but also contains smaller amounts of natural gas liquids like ethane, propane, and butane, along with small quantities of non-hydrocarbon gases.

Natural gas is termed “natural” because it occurs in nature and is not synthetically manufactured – unlike gas produced from coal (often called town gas or coal gas) – it is extracted directly from underground deposits in the environment. So, while referred to as ‘natural’, it is nonetheless a fossil fuel and not renewable on a human timescale. Any combustion of natural gas adds fossil carbon dioxide to the atmosphere, contributing to climate change.

In 2024 the UK’s natural gas demand fell to the lowest level since 1992 with declining demand largely due to reduced consumption in electricity generation. Over the last quarter of a century gas demand for electricity generation has been in general decline, reflecting an overall drop in total electricity generation and the increasing share of renewable power from wind and solar energy. In 2024, electricity generation represented 26% of total gas demand.

Additionally, 2024 saw UK natural gas production at its lowest level since 1973. Gas production dropped 10 per cent from the previous year following the expected decline in production from the UK’s mature North Sea basin.

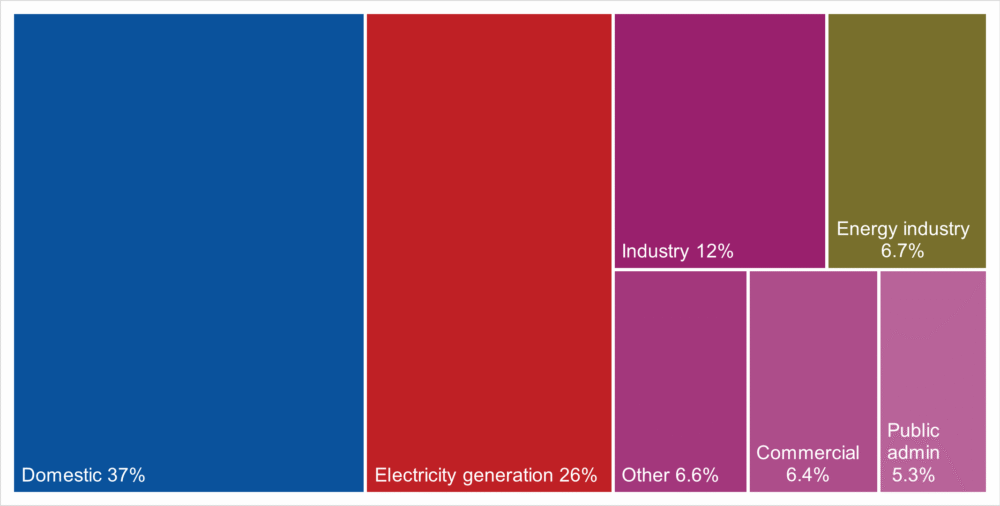

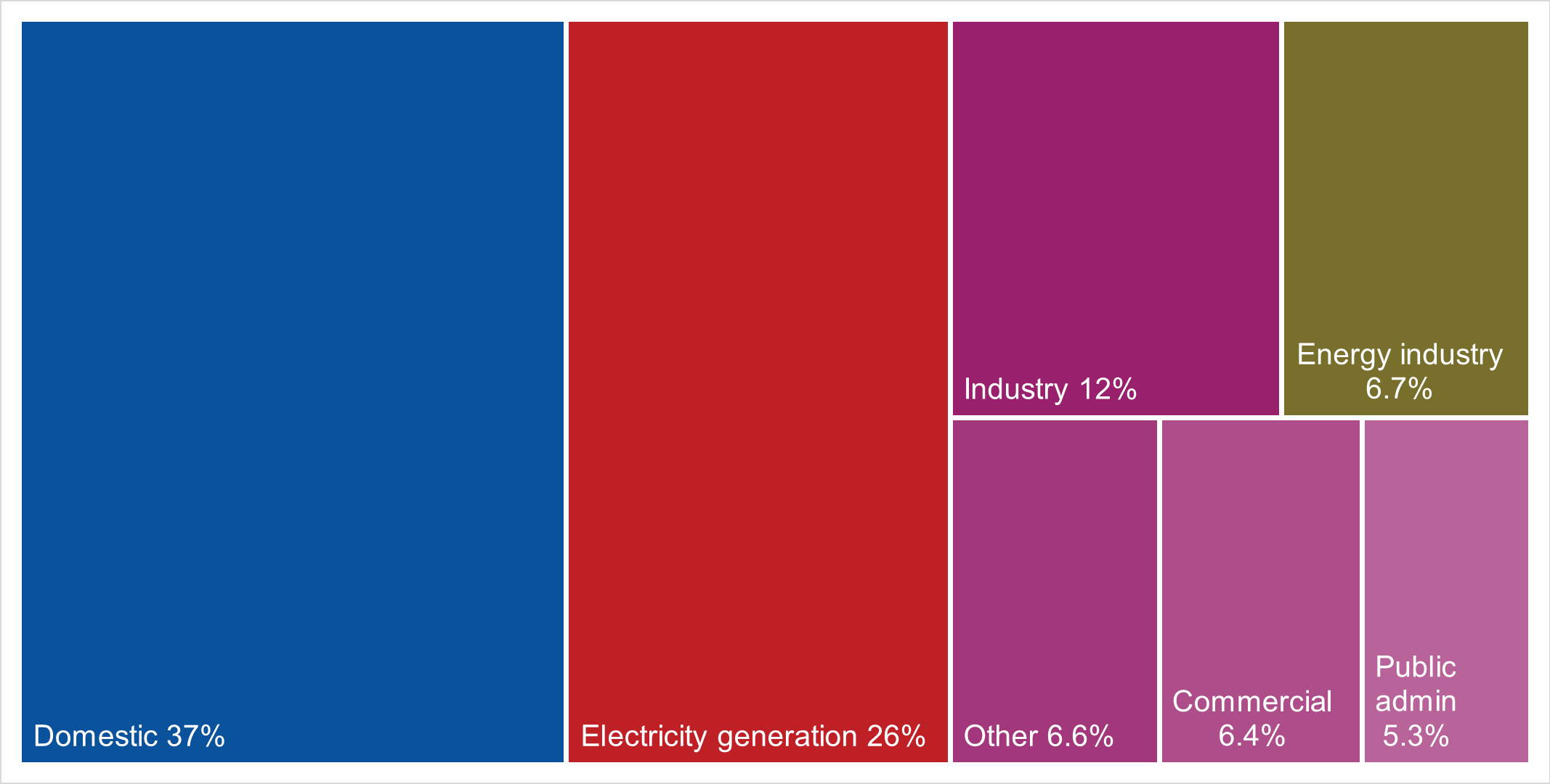

Although power generation continues to use a substantial—though decreasing—amount of natural gas, its main application is for heat production (Figure 1). Domestic heating represented 37% of demand in 2023-24, with around 21.2 million (86%) households using a gas fired main heating system to heat their home.

Historically the volume of domestic gas consumption has been driven by temperature and gas prices, with high prices driving down gas use and low temperatures pushing consumption up. The last few years have seen a combination of high temperatures and high prices reducing demand to below the 2017-2021 average. However, future domestic gas demand is expected to gradually reduce due to the roll out of heat pumps as part of the government’s net zero strategy.

Figure 1. UK Natural Gas Consumption by sector (2024) (Source: Digest of UK Energy Statistics).

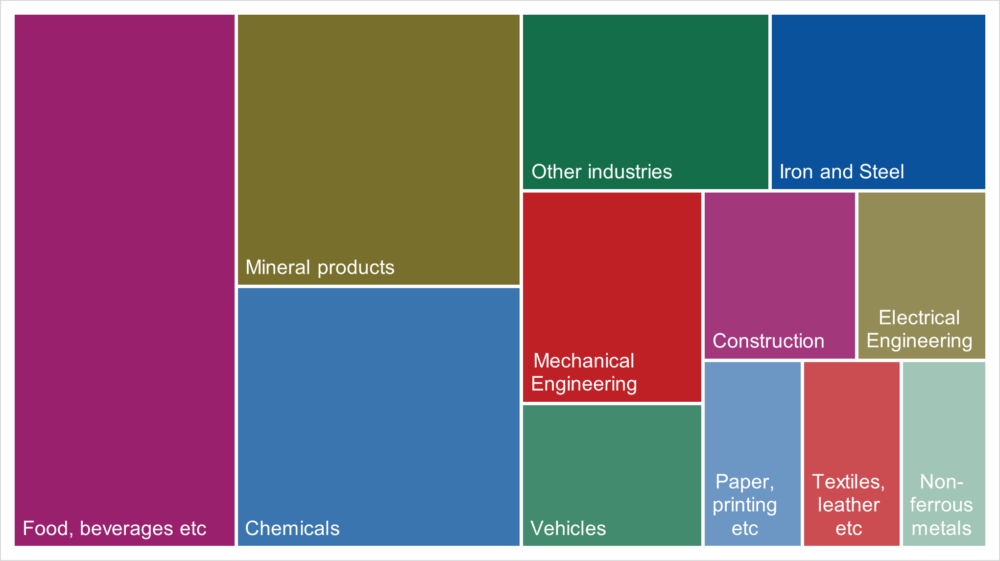

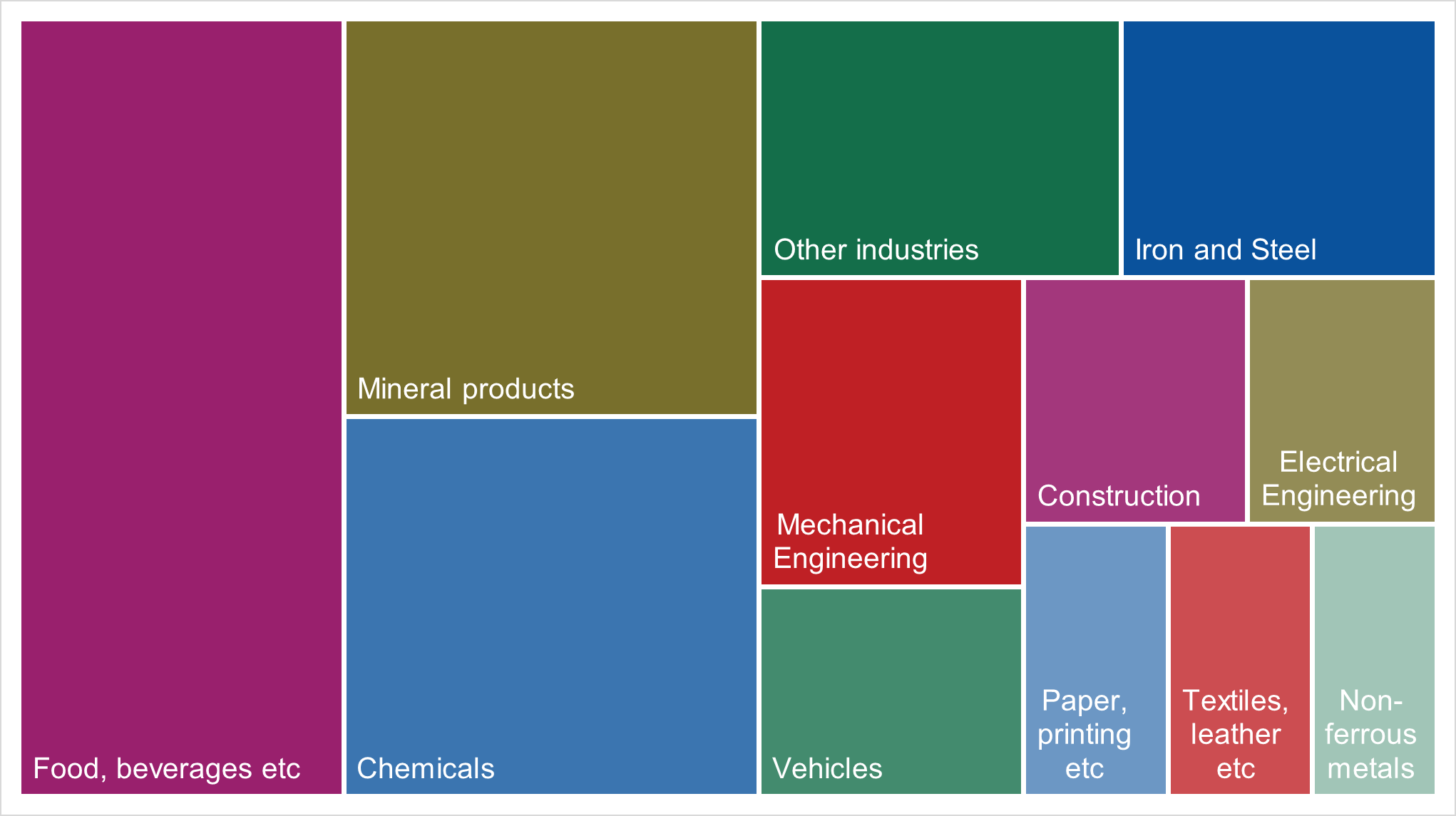

Figure 2. UK industrial natural gas consumption by sector (2024) (Source: Digest of UK Energy Statistics).

The consumption of gas in commercial and public sectors follows a similar pattern to domestic consumption. Industrial demand has decreased over the last five years due to energy efficiency gains and the decline in UK based energy intensive manufacturing (Figure 2).

Although natural gas is predominantly used as fuel it is also a source of carbon in chemical manufacturing. As an example, Ineos Acetyls operate Europe’s largest acetic acid plant at the Saltend Chemicals Park on the Humber estuary. Ineos’s advanced Cativa™ process converts natural gas to carbon monoxide which is reacted with methanol to produce acetic acid. The site has the capacity to produce 500,000 tonnes of acetic acid representing a methane demand of around 2.5TWh as a chemical feedstock.

The rising production of biomethane.

As stated earlier, whilst natural gas is a fossil fuel, its molecular twin – biomethane – is a renewable version produced through anaerobic digestion. Anaerobic digestion (AD) is a biological process that breaks down organic materials, such as food waste, sewage sludge, manure, crops, and crop residues, in an oxygen-free environment. Microorganisms decompose these materials through a series of biological reactions, producing biogas. This biogas typically comprises 50–70% methane and 30–50% carbon dioxide, with trace amounts of other gases. The solid or liquid by-product, known as digestate, is commonly used as a fertiliser, providing nutrients and organic matter to soil and crops, much like manure. A process known as biogas upgrading is used to sperate the methane from carbon dioxide and other gases, producing a methane suitable for injection into the gas network or direct use as a transport fuel.

The rise in biomethane production has been driven by supportive government policies. Under the Renewable Heat Incentive (RHI), the volume of biomethane placed on the grid increased substantially between 2011 and 2023, from under half a million to over 400 million m3 per annum.

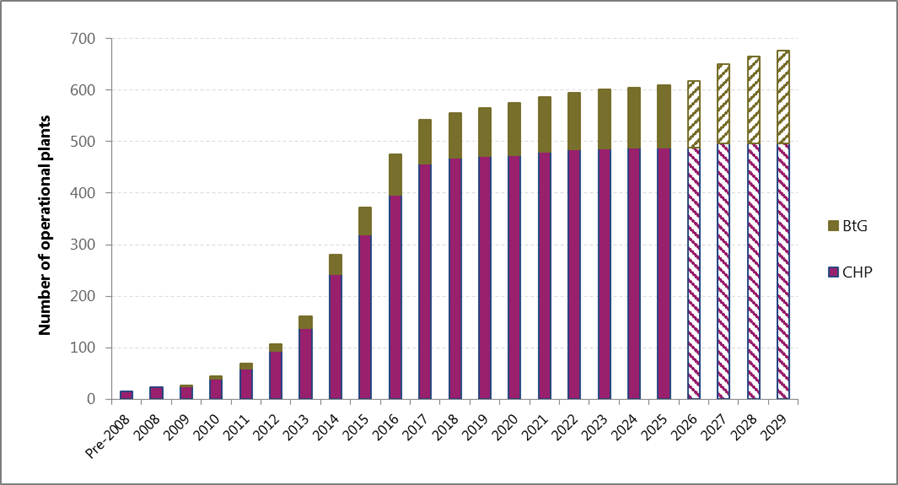

Figure 3: Cumulative number of Biomethane to Grid (BtG) AD plants (excluding water treatment plants) (2026-2029 forecasted) (Source: Alder BioInsights)

As of 2025, approximately 600 AD facilities were operational in the UK. The number of facilities upgrading biogas to biomethane for injection into gas network (known as biomethane to grid (BtG) plants) exceeds 120, providing a total production capacity of over 7 TWh and an injection capacity in excess of 11 TWh. With biomethane production now benefiting from a Green Gas Support Scheme (GGSS) and a future biomethane policy framework planned, the growth in biomethane production is set to continue with an estimated 70 biomethane to grid projects under development in the UK.

Currently biomethane production represents a fraction of methane supply, but in a declining methane market, how significant could biomethane be, as a share of total methane supply?

In respect to demand, the UK’s National Energy System Operator’s (NESO) future energy scenario pathways consider different ways Great Britain can reach a net zero energy system. In a ‘falling behind’ scenario where some decarbonisation progress is made but insufficient to meet net zero natural gas demand would remain high at 640TWh and the contribution of biomethane would remain modest. However, within scenarios designed to meet net zero either through a focus on electrification, hydrogen or a combination of the two – methane demand ranged between 98 and 328TWh (with the higher demand in the hydrogen focused scenario), and biomethane’s contribution was stated at 64TWh which is a vast increase on today.

Ultimately, Government policies will determine how successful the continued scale up of biomethane supply will be and it has always been anticipated that the availability of sustainable biomass could constrain supply. However, anaerobic digestion can process a wide variety of feedstocks from food waste to dedicated rotational crops and recent work by Alder for the Green Gas Taskforce (GGT) has shown there is the potential to produce up to 120TWh of sustainable biomethane based on domestic feedstocks alone.

Building a sector on a secure, stable and sustainable feedstock supply is fundamental and at Alder BioInsights we have developed unrivalled feedstock knowledge, underpinned by an internal database covering all types. We also have extensive knowledge of feedstock procurement, management, use and sustainability. This enables us to advise early stage or operational developments to make the best business decisions, to deliver the most favourable environmental and economic outcomes. The feedstock market is changing, and the future landscape is expected to look quite different to what we see today, so navigating this transition is key to the future success of the sector.

As bioeconomy consultants, we are also monitoring market developments across all sectors and consider the best use of biomass, resultant energy or molecules that could prove valuable across the breadth of the bioeconomy.

Anaerobic Digestion Deployment in the UK 2025, Alder BioInsights, April 2025.

Digest of UK Energy Statistics (DUKES) 2025, Department for Energy Security and Net Zero, July 2025.

Future Energy Scenarios – Pathways to Net Zero, National Energy System Operator, November 2025.

Hydrogen heating: overview, Department for Energy Security and Net Zero, December 2024.

Ineos Acetyls – Hull, Ineos, Accessed March 2026.

Net Zero Strategy – Build Back Greener, Department for Energy Security and Net Zero, October 2021.